DeFi is known for its high yields. It’s not exactly known for its stability. This creates a structural friction for crypto adoption for real financial use cases, because borrowing requires a stable cost of money.

In DeFi there are a lot of crypto lenders, but there are no real borrowers. Borrowers borrow to invest in a capital asset, to buy a house, to finance living activity, etc. Borrowing simply to lend again (eg a yield farm) is what a financier does. There are a lot of financiers in DeFi, there are basically no true borrowers.

This isn’t because there’s no market for borrowing. It’s because DeFi’s lending options are far too volatile for it. During bull markets demand for leverage skyrockets, sending yields up, and vice versa in crypto winters. You can’t depend on this caprice for economic loans. Almost no one can reasonably make a capital investment where the cost of debt can have regular 1,000-basis-point swings.

A solution: offer fixed rates. However because of the volatility in DeFi money markets, getting a fixed rate often means you get a delta between fixed and floating that isn’t economically tolerable. During the bull run, I recall seeing Aave’s USDC floating rate around 3%, and the fixed was almost 12%. Right now it’s about 1.5% and 5.5%, respectively. The market for fixed rates is well aware of the violent moves and is priced accordingly.

The reason for this is money markets were never meant to be used for medium-to-long-term funding. DeFi currently has a volatile short-term rate attempting to solve a stable long-term need.

Enter the yield curve and term structure.

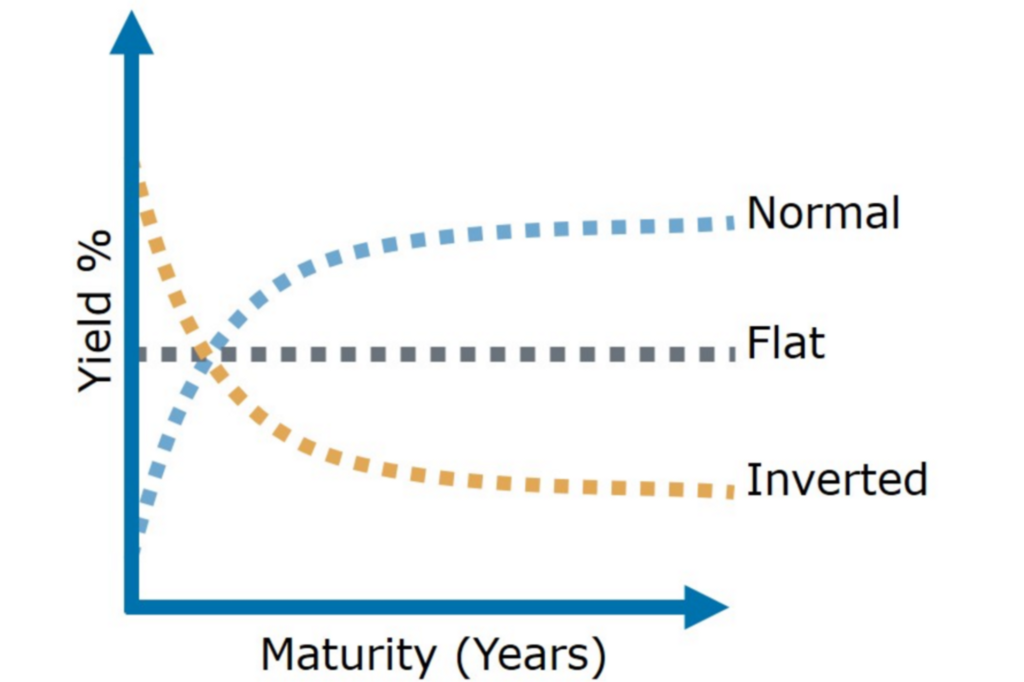

Yield curve: a visual representation of debt yield at different maturities. It shows the point-in-time yield on debt that investors expect. Conversely, it also lets borrowers know what yields are needed to attract investment.

Term structure: references the slope of the yield curve across these different maturities. All things being equal, debt with longer maturity pays a higher yield. However that is not always how markets price risk for varying reasons (this is discussed in more detail in my yield-curve dissection here). Term structure can take on various shapes, as seen below.

Money markets cannot adequately capture this term structure. A fixed-rate money market yield doesn’t encapsulate that rates should be different based on the term of the loan. Costs of debt must be priced over time to foster true-borrowing activity. DeFi needs to find a real cost of crypto money across medium (3-12 months) and long-term (>12 months) time frames. DeFi needs a yield curve.

The most expedient path for this is simply borrowing rates from TradFi. DeFi could take the curve that exists in other financial products like futures and bonds, and price fixed-rate loans based off those instruments and their corresponding terms. This effectively would be importing the term structure of TradFi products onchain. As crypto matures, we can rely less on these external rates or use them to augment crypto-native pricing.

Is anyone in DeFi trying to cater to true borrowers? Let’s review the top-5 undercollateralized lending apps and who their target markets are. None of the following is an endorsement of any DeFi app or a recommendation to invest in anything. In order of total value locked (TVL):

1. Maple Finance: $125M TVL

Maple is an institutional capital marketplace that takes deposits onchain and provides loans to institutions offchain. Users deposit crypto into lending pools that are subject to a 90-day lockup period and then 10-day processing request. So effectively lending to Maple is a minimum 100-day term. Borrowers are all whitelisted institutional industry professionals with credit experience.

Maple is facilitating medium-term crypto-native lending, however the institutional focus means it’s likely for financier activity. Borrowers are likely hedge funds that are redeploying it back into the market. There’s not a true-borrower intent here, but still a step in the right direction.

2. Gearbox: $115M TVL

Gearbox is a leveraged farming app. It has two sides to it: passive liquidity providers, and active borrowers who can borrow with up to 10x leverage.

Gearbox lets you borrow multiples of your deposited collateral with the explicit intent to use it across DeFi apps for yield farming. So all the borrowing stays onchain and for financier purposes, not true borrowing.

3. Goldfinch: $100M TVL

Goldfinch is a credit app whose stated mission is to bring the world’s credit activity onchain. They provide crypto loans without requiring crypto collateral. They use a concept described as “trust through consensus” for borrowers to show creditworthiness based on collective assessment, rather than rely on collateralizing with crypto.

They target emerging-market lending institutions as their main clients. These borrowers propose deal terms for credit lines, and DeFi users can then supply crypto for a yield.

The emphasis on emerging markets is compelling. Several of the clients they cite in their docs are lending businesses that provide capital to individuals for what appears to be real-life borrowing. Their focus is getting capital to under-served businesses and communities, this seems like a true-borrowing facilitator.

4. Clearpool: $58M TVL

Clearpool bills itself as a DeFi ecosystem with the first-ever permissionless marketplace for unsecured institutional liquidity. They let institutions raise short-term capital and provide DeFi lenders access to returns based on interest rates derived from “market consensus”. They offer both permissioned and unpermissioned pools, both intended for institutional lending.

Similar to Maple, Clearpool is providing offchain lending based on onchain assets for financiers. The emphasis on institutions and short-term capital confirms as much.

5. Centrifuge: $83M TVL

Centrifuge describes itself as a network that provides access to fast, cheap capital for small businesses, claiming they allow anyone to launch an onchain credit fund creating collateral-backed pools of loans.

Centrifuge’s explicit aim per their docs is “to bring down the cost of capital for SMEs and provide DeFi investors with a stable source of yield uncorrelated from volatile crypto assets”. Continued: “Asset pools are fully collateralized, liquidity providers have legal recourse, and the protocol is asset-class agnostic with pools for assets spanning mortgages, invoices, microlending and consumer finance.”

Helping small businesses and lending for real-world activity like mortgages and invoices? This market very much speaks to true borrowing! I’m encouraged to see the activity Centrifuge and Goldfinch are trying to facilitate.

The more DeFi builds to cater to real economic investment, the quicker we’ll find our yield curve. Keep tracking this space and reach out if you come across any cool projects along these lines.

Follow at @BackTheBunny

Check out another popular posts --> Predicting Recessions: What Yield Curves Tell Us About the Future Demand for Money

Comments are closed!